All Categories

Featured

Table of Contents

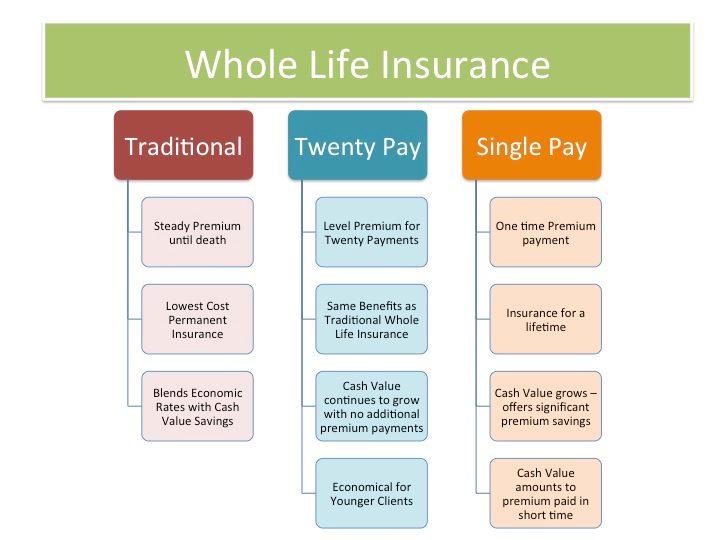

The are entire life insurance policy and global life insurance coverage. expands cash money worth at a guaranteed interest rate and additionally via non-guaranteed rewards. expands cash value at a taken care of or variable rate, depending upon the insurance company and policy terms. The cash money value is not contributed to the survivor benefit. Cash money value is a function you make use of while active.

The plan financing rate of interest price is 6%. Going this path, the passion he pays goes back right into his policy's cash money value instead of a financial establishment.

Visualize never having to stress concerning financial institution car loans or high rate of interest prices once again. That's the power of unlimited financial life insurance.

There's no collection car loan term, and you have the freedom to select the repayment routine, which can be as leisurely as paying off the loan at the time of fatality. This adaptability includes the servicing of the fundings, where you can select interest-only payments, keeping the funding balance level and convenient.

Holding money in an IUL fixed account being credited passion can usually be better than holding the cash on down payment at a bank.: You've constantly imagined opening your own pastry shop. You can borrow from your IUL plan to cover the first expenditures of leasing a space, purchasing devices, and working with staff.

Infinite Banking Think Tank

Personal loans can be gotten from conventional financial institutions and credit report unions. Borrowing cash on a debt card is typically really costly with yearly percentage rates of interest (APR) commonly reaching 20% to 30% or even more a year.

The tax therapy of policy loans can vary significantly depending on your nation of residence and the details terms of your IUL plan. In some areas, such as North America, the United Arab Emirates, and Saudi Arabia, plan financings are normally tax-free, using a considerable benefit. In various other jurisdictions, there might be tax implications to think about, such as possible taxes on the car loan.

Term life insurance coverage only provides a death benefit, with no cash worth buildup. This indicates there's no cash value to obtain against. This short article is authored by Carlton Crabbe, President of Capital permanently, a professional in supplying indexed global life insurance policy accounts. The information provided in this post is for educational and informative purposes only and ought to not be taken as financial or financial investment advice.

Infinite Banking Concept Canada

When you first listen to about the Infinite Banking Concept (IBC), your very first reaction may be: This seems too good to be real. The trouble with the Infinite Financial Principle is not the principle but those persons providing an adverse review of Infinite Financial as a concept.

So as IBC Authorized Practitioners through the Nelson Nash Institute, we thought we would certainly answer a few of the leading inquiries individuals search for online when finding out and recognizing everything to do with the Infinite Financial Idea. What is Infinite Financial? Infinite Financial was produced by Nelson Nash in 2000 and totally discussed with the magazine of his publication Becoming Your Own Banker: Unlock the Infinite Financial Concept.

Infinite Banking

You assume you are coming out monetarily in advance due to the fact that you pay no interest, but you are not. With saving and paying cash money, you may not pay rate of interest, yet you are using your cash as soon as; when you invest it, it's gone for life, and you offer up on the possibility to make life time substance rate of interest on that money.

Even banks make use of whole life insurance for the same purposes. The Canada Income Firm (CRA) also acknowledges the worth of participating entire life insurance coverage as an unique asset class utilized to generate long-term equity securely and predictably and supply tax obligation benefits outside the scope of conventional investments.

How To Start Infinite Banking

It enables you to generate wide range by meeting the financial feature in your very own life and the capability to self-finance major way of life acquisitions and expenses without disrupting the compound passion. Among the easiest methods to think of an IBC-type taking part entire life insurance policy policy is it approaches paying a home loan on a home.

Over time, this would certainly create a "consistent compounding" impact. You obtain the photo! When you borrow from your getting involved whole life insurance coverage policy, the money value proceeds to expand continuous as if you never ever borrowed from it in the first place. This is because you are using the money worth and survivor benefit as security for a funding from the life insurance firm or as collateral from a third-party lending institution (recognized as collateral financing).

That's why it's vital to deal with a Licensed Life insurance policy Broker licensed in Infinite Financial who frameworks your getting involved entire life insurance policy correctly so you can avoid adverse tax implications. Infinite Banking as a monetary technique is not for every person. Here are a few of the advantages and disadvantages of Infinite Financial you ought to seriously consider in determining whether to move on.

Our recommended insurance policy carrier, Equitable Life of Canada, a shared life insurance company, specializes in participating whole life insurance policy policies details to Infinite Banking. Likewise, in a shared life insurance coverage company, policyholders are considered company co-owners and get a share of the divisible excess produced every year through returns. We have a range of providers to pick from, such as Canada Life, Manulife and Sun Lifedepending on the demands of our clients.

Please also download our 5 Top Inquiries to Ask A Boundless Financial Representative Prior To You Work with Them. For additional information about Infinite Banking visit: Please note: The product given in this newsletter is for informative and/or academic functions just. The info, point of views and/or sights shared in this e-newsletter are those of the authors and not always those of the supplier.

Bank Of China Visa Infinite Card

The principle of Infinite Banking was developed by Nelson Nash in the 1980s. Nash was a finance professional and follower of the Austrian school of business economics, which promotes that the worth of items aren't explicitly the result of standard financial structures like supply and need. Instead, people value cash and goods differently based upon their financial standing and needs.

Among the challenges of standard financial, according to Nash, was high-interest prices on finances. Way too many individuals, himself included, entered economic trouble due to dependence on banking organizations. Long as financial institutions set the interest prices and car loan terms, people didn't have control over their very own wide range. Becoming your very own banker, Nash determined, would put you in control over your monetary future.

Infinite Financial needs you to have your monetary future. For goal-oriented people, it can be the most effective economic device ever. Right here are the advantages of Infinite Financial: Perhaps the solitary most beneficial element of Infinite Financial is that it improves your capital. You don't require to undergo the hoops of a typical financial institution to obtain a financing; simply request a policy lending from your life insurance policy business and funds will be offered to you.

Dividend-paying entire life insurance policy is extremely low danger and offers you, the insurance holder, a lot of control. The control that Infinite Financial uses can best be grouped right into two classifications: tax benefits and asset securities. Among the reasons whole life insurance policy is ideal for Infinite Banking is how it's taxed.

Whole life insurance plans are non-correlated assets. This is why they function so well as the economic structure of Infinite Banking. Regardless of what happens in the market (supply, real estate, or otherwise), your insurance plan retains its worth.

Market-based financial investments grow wealth much faster but are revealed to market changes, making them inherently high-risk. What happens if there were a third container that used safety yet additionally modest, guaranteed returns? Whole life insurance coverage is that third bucket. Not only is the rate of return on your whole life insurance policy plan assured, your survivor benefit and premiums are likewise guaranteed.

Royal Bank Infinite Avion

Infinite Banking charms to those seeking better economic control. Tax obligation effectiveness: The cash worth expands tax-deferred, and policy financings are tax-free, making it a tax-efficient device for developing riches.

Possession protection: In many states, the cash money value of life insurance policy is shielded from financial institutions, adding an added layer of financial safety. While Infinite Financial has its values, it isn't a one-size-fits-all option, and it includes substantial drawbacks. Right here's why it may not be the best strategy: Infinite Financial often needs elaborate plan structuring, which can confuse policyholders.

{kind=link}

Latest Posts

Cash Flow Banking Insurance

Infinite Insurance And Financial Services

How Do I Start My Own Bank?